Operational Considerations

- Preserving capital efficiency

- Managing risk exposure

- Avoiding liquidation when operating leveraged or JIT-powered LPs

The interface serves as a tool for manipulating parameters to achieve desired results rather than making risk recommendations. Operators must independently assess and manage their risk tolerance based on market conditions and their specific strategies.

EulerSwap's JIT model automatically borrows assets to fulfill swap requests, making the protocol highly capital efficient while requiring careful monitoring of debt positions and collateral ratios

Price Divergence Management

When current price increases above equilibrium (for example, WETH/USDC rising), the LP may accumulate excess WETH debt and should consider rebalancing to maintain neutrality. This price divergence triggers borrowing in the JIT model, as EulerSwap uses dynamic on-chain execution to satisfy swaps by borrowing output tokens against input token collateral.

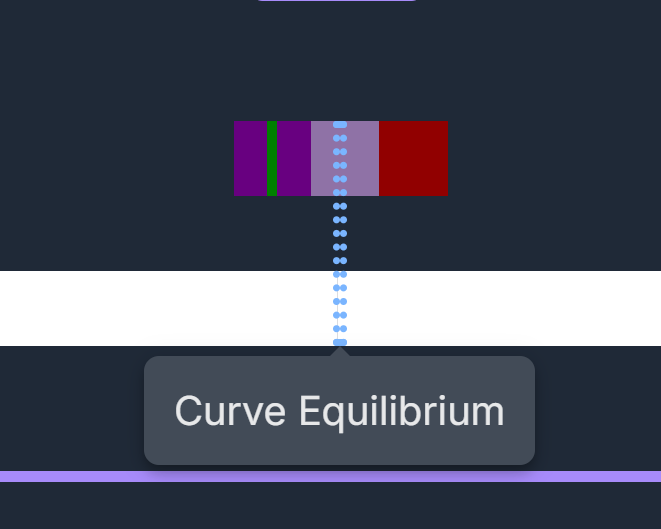

Price at Equilibrium (Green Bar):

The marginal price where the AMM curve is centered, representing the theoretical balance point where virtual reserves of both assets are aligned. This equilibrium price is defined by priceX and priceY parameters when setting up the pool and determines the AMM curve's slope at the midpoint

Current Price (Blue Bar):

The real-time market price based on active trading or external references like oracles. When current price diverges from equilibrium, it indicates directional exposure, more of one asset is held or borrowed than the other